Annual Report 2024-25

Letter of transmittal

22 September 2025

The Hon. Tom Koutsantonis MP

Treasurer of South Australia

Parliament House

North Terrace

Adelaide SA 5000

Dear Treasurer,

HomeStart’s 2024–25 Annual Report

I am pleased to present a summary of HomeStart’s achievements over the 2024-25 financial year.

HomeStart provided a record $1.4 billion in new loans to 2,923 home buyers, bringing the total number of South Australians helped by HomeStart to more than 91,000.

This is my final report as Chair of the HomeStart Board. It has been a privilege to support HomeStart in its purpose to help more people into home ownership in more ways.

Should you have any questions about the report, I would be pleased to provide you with further information.

Yours sincerely,

Jim Kouts | Chair

Message from the Chair

Jim Kouts

Strong institutions play a critical role in the economic development of the state and HomeStart continues to have a formidable capacity to deliver both for its customers and the South Australian community. As I step down as Chair, my final report gives me pause to reflect on the long-term achievements of this most beloved and respected South Australian institution.

Emerging from the global financial crisis in 2010, the value of HomeStart’s new lending was $472 million. The business rebounded through the next decade and faced the challenge of COVID head on. With low interest rates not seen since the 1960s, one could ask why we needed an institution such as HomeStart when mainstream finance was readily available.

Yet, as housing affordability has since worsened, HomeStart has played a significant role in helping South Australians buy a home when they couldn’t access mainstream finance - and this past financial year has been no different.

Amid one of the most challenging housing markets, this year we provided $1.4 billion in new loans. Of utmost importance, 2,923 loans were delivered seamlessly. HomeStart’s pre-tax underlying profit of $48.1 million and headline profit of $65.1 million were both higher than the prior year. Since 2010, our portfolio value has risen from $1.7 billion to $3.6 billion.

In 2010, we returned $20.8 million to the State Government and in 2024-25 we contributed $100.6 million. This brings our total contribution since HomeStart’s inception to more than $1.1 billion, which is vital for the state economy.

Most importantly, throughout its 35-year history, HomeStart has helped more than 91,000 South Australians into home ownership. We have stood true to our values, remained committed to our purpose, and made the dream of home ownership a reality for more people in more ways.

Today, we are in the midst of a complex housing market where the interest rate cycle has reversed, cost-of-living pressures continue, housing supply remains a challenge and house prices continue to rise.

The scale and complexity of HomeStart’s role has grown significantly and our financials paint a picture of sound long-term decisions.

HomeStart proudly delivers on its purpose within a commercial framework. While our offering to customers is unique and flexible, we uphold responsible lending practices. Good corporate governance is critical to this balance. HomeStart’s governance model continues to underpin its organisational success.

Our results demonstrate the increasing community need for HomeStart’s support. Significant economic challenges remain ahead. As South Australia responds to the national housing crisis through the State Government’s Housing Roadmap, it will be critical that the independence of HomeStart’s framework allows it to continue to deliver on its remit.

Among the ingredients of a strong organisation is a sustainable policy on dividends and capital and the maintenance of a skilled Board.

As I conclude my term as Chair, HomeStart has farewelled two highly-capable business people in long-serving Deputy Chair Chris Ward and Board Member Sue Edwards. I offer my personal thanks – and that of the entire Board – for their outstanding contributions to HomeStart.

I have served 12 years as Chair of HomeStart’s Board after an apprenticeship as Deputy Chair. As my stewardship of HomeStart comes to completion, I thank the various Ministers and Treasurers and their teams who have supported the business.

HomeStart is all about people – the people of South Australia, our diverse customers, and our passionate HomeStart team. I would particularly like to acknowledge the considered leadership of CEO Andrew Mills and his executive team, his predecessors, and the entire HomeStart workforce, who have been relentlessly committed to breaking down barriers to home ownership for South Australians.

Owning a home is important to financial security and it has been an absolute privilege to help tens of thousands of South Australians to achieve their home ownership dream.

Jim Kouts | Chair

Message from the CEO

Andrew Mills

The dream of buying a home remains a challenge, and HomeStart’s results tell a compelling story of delivering for the community in a time of genuine need. Economic forces in the past year included cost-of-living pressures, South Australian house prices reaching unprecedented levels, and a turning point in the interest rate cycle. Through these conditions, HomeStart’s strengths facilitated another year of record lending.

In the 2024-25 financial year, HomeStart proudly helped 2,923 home buyers – including 1,803 first home buyers - into home ownership. A significant portion of lending supported new housing supply, with 1,424 construction-related loans. Our overall lending value was a record $1.4 billion.

Our results continue to prove shared equity’s important role as a means of helping people into home ownership. We provided a record 1,170 additional loans through our Shared Equity Option, a 32% increase on the previous year. More than 40% of new customers benefited from shared equity.

Importantly, 173 customers paid out the shared equity portion of their loan, most commonly by refinancing to another lender. HomeStart’s model recognises that once customers have built equity, refinancing can be a positive next step, and several initiatives were introduced this year to better inform customers about refinancing pathways.

Total discharges reached a record $826 million, up 93%, with 88% of this total due to refinancing. Many customers expressed pride in “paying it forward”, knowing their repayments would help other South Australians into home ownership.

Portfolio credit quality remained strong through the year and our 90-day arrears rate remained low at 0.33%.

At an operational level, we launched a new loan origination system, and I wish to thank all involved in this long and complex project.

Significant improvements in service to borrowers and brokers has been achieved as a result, with substantial improvement in our ‘time to yes’ measure, as well as introducing digital loan application capability. Many home buyers prefer to use mortgage brokers, who play an important role in helping us reach more South Australians. In the past financial year, 79% of new lending occurred via brokers, an increase of 9%.

This year’s results are a reflection of our employees, and I thank the entire HomeStart team for their hard work, commitment to our purpose, and care for our customers and each other. We have built an environment where people feel they can speak up, illustrated by the 91% participation rate in our engagement survey, and a further lift in our engagement scores.

As we look towards another challenging year, I thank the Treasurer and his team for their continued support of HomeStart. I also thank my Executive team for their leadership and support, and join our Chair in thanking outgoing Deputy Chair Chris Ward and Board Member Sue Edwards for their valued contribution to the HomeStart Board. Lastly, I would like to acknowledge and thank Chair Jim Kouts for his outstanding service to the Board, and particularly as Chair since 2013.

Each day we are privileged to be a part of another South Australian home buyer’s story. Behind every loan are the hopes and dreams of people who want to own a home. We are fortunate to be a part of their journey. All who work within and in partnership with HomeStart should be proud of the difference we make for so many South Australians. More than 91,000 South Australians have now had a home to call their own, thanks to HomeStart. We look forward to helping many more in the coming years.

Andrew Mills | Chief Executive Officer

Customer

| 2,923 New loans |

| 1,803 First home buyers |

| 49% New loans were construction-related |

| $494,335 Average loan value |

Financial

| $48.1M Underlying profit |

| $3.6BN Portfolio |

| $1.4BN Total lending |

| $100.6M Contributed to State Government |

Process

| 2,858 Loans discharged |

| $826M Loans repaid by customers discharging |

| 79% Loans via Brokers |

| 0.33% 90-day arrears rate |

People

| 91% Participation in employee engagement survey |

| 0 Lost time injury days |

| 55% Female employees |

| 100% Employees had a performance development discussion recently |

Repayment Safeguard

A unique benefit of all HomeStart loans is the Repayment Safeguard. It sets our customers’ repayments at an affordable level from the start of the loan.

The repayments are then only adjusted once every 12 months in line with inflation, not when interest rates change. The certainty of our Repayment Safeguard makes it easier for customers to budget and manage finances once a home is purchased.

Customer and community impact

Customer experience

77% Customer Experience Score for FY 2024-25

37% Improvement in Time to Yes (YoY)

74% Broker Satisfaction Score for FY 2024-25

36 Net Promoter Score for FY 2024-25

Community engagement

Seminars

HomeStart provides free educational seminars to help participants gain the knowledge, tools, and confidence to begin their journey toward buying or building a home.

7 Home Buyer Seminars

393 Attendees

Home Buyer Ready program

Home Buyer Ready provides information to help customers get started to buy or build their own home, such as how to budget and save for a deposit, understand the costs involved, how to work out how much they can borrow and what their repayments might be.

2,812 Users

679 Modules completed

Community partnerships

|  | ||

Member and Community Partner | Fashion and Costume Parade Naming Rights Partner | Naming Rights Partner for Family Zone and Presenting Partner for Free CBD Shuttle | Scholarship Sponsor |

Donations

HomeStart proudly partnered with Habitat for Humanity SA, volunteering our time and contributing $6,016 to help create safer spaces for those in need. In total, we donated $7,266 during FY 2024–25, demonstrating our commitment to building stronger communities.

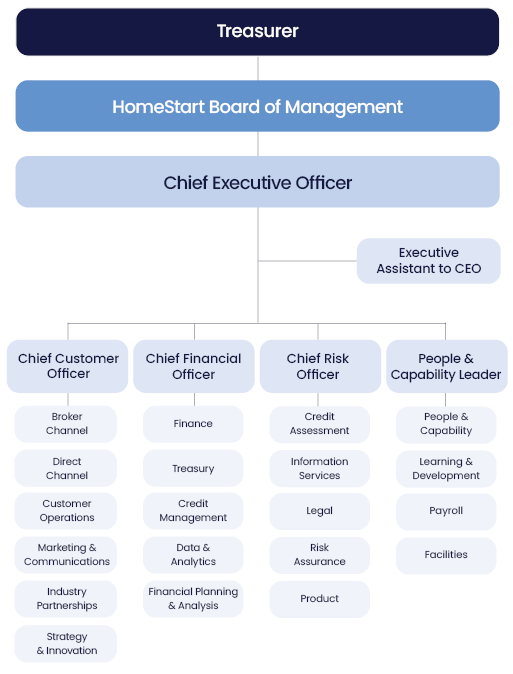

Organisation chart

Our Board

| Jim Kouts | ChairJim Kouts has significant commercial, strategic and governance experience across a range of national and state based private and government sector organisations. He is a former senior national executive having worked for two global energy groups for close to 20 years. Jim is Deputy Chair and Non-Executive Director of the Adelaide Economic Development Agency, and a Non-Executive Director of Business Events Adelaide (BEA). Until recently he was Chair of BEA. He is also a Non-Executive Director of the Adelaide Venue Management Corporation and a long-term strategic adviser to both Adelaide Airport Limited and Flinders Port Holdings. Jim was appointed Chair of HomeStart in December 2013, having previously been Deputy Chair. |

| Chris Ward | Deputy ChairChris Ward is a professional Non-Executive Director, having had more than 30 years of broad executive experience, primarily in banking and finance. He is an Advisory Board Chair to two private companies. Chris is a former Non-Executive Director, Chair of the Risk and Audit Committee, and member of the Remuneration Committee at the South Australian Film Corporation, a former Non-Executive Director of the Australian Dance Theatre and was an Executive Partner at UniSA. Chris was appointed to the HomeStart Board in June 2012, appointed Deputy Chair in December 2013 and was Chair of the Asset and Liability Committee (ALCO). Chris completed his term on the Board in June 2025. |

.jpg) | Andrew Seaton | Board MemberAndrew Seaton is Managing Director and Chief Executive of Australian Naval Infrastructure. He has extensive finance, strategy, commercial and project management experience, having worked in banking, natural resources and defence industries for more than 35 years. Andrew previously held the roles of Chief Financial Officer at Santos Limited, Vice-President Investment Banking with Merrill Lynch and Client Director with NAB. He is a Non-Executive Director of ASX-listed Strike Energy Ltd. Andrew was appointed to the HomeStart Board in 2019 and is the Chair of the Audit and Risk Committee. |

| Shanti Berggren | Board MemberShanti Berggren is the General Counsel and Executive Director of Legal Services at the University of Adelaide. She is a commercial lawyer who has worked in private practice and in-house roles in Los Angeles, Singapore, and Sydney. She is also a Director of the Adelaide Football Club. Shanti was appointed to the HomeStart Board in March 2017. |

| Sue Edwards | Board MemberSue Edwards is a chartered accountant and is currently a Director of Mitolo Family Farms and Executive Officer of the Mitolo Family Office. She is a former Partner at Deloitte where she specialised in providing business advice, including strategy, finance and taxation, and is a former treasury manager. Sue Edwards was appointed to the HomeStart Board in December 2010. Sue completed her term on the Board in December 2024. |

| Stella Thredgold | Board MemberStella Thredgold brings extensive experience from her career as an experienced ASX 100 C-Suite executive with national responsibilities specialising in the banking, superannuation and finance industry. She consults and advises on leading organisations through change with experience in delivering complex transformations relating to strategy, risk and compliance, customer experience, technology, people, organisational culture, digital transformations and corporate governance. Stella is also a Non-Executive Director of Discovery Parks, and Slater & Gordon. Stella was appointed to the HomeStart Board in February 2024. |

.jpg) | Richard Bryant | Board MemberRichard Bryant brings with him more than 40 years of leadership experience in the property, construction, and engineering sectors, holding high-level strategic and general management roles. His career has seen him establish and oversee businesses throughout Australia, where he has applied his considerable expertise in formulating and implementing business strategies, organisational structures, staffing, and operational systems. Additionally, Richard has contributed his leadership to various board roles within both the commercial and not-for-profit sectors. Richard was appointed to the HomeStart Board in May 2024. |

Our Executive team

| Andrew Mills | Chief Executive OfficerAndrew Mills became Chief Executive Officer in January 2022, having previously held senior executive positions across the organisation over the past decade. He possesses strong financial and business acumen and has been a key contributor to the success of HomeStart, fostering strong relationships within the organisation and externally. Andrew brings a unique focus on product innovation, digital transformation and organisational development, which is instrumental in leading HomeStart through this challenging time in the housing market. His commitment to help more South Australians into home ownership is coupled with a belief that HomeStart can continue to play a key role in the economic and social prosperity of the State. |

| Vas Iannella | Chief Customer OfficerVas Iannella joined HomeStart in May 2020 as Chief Customer Officer, bringing more than 15 years of experience in retail and commercial banking. Throughout her career, Vas has been instrumental in transforming customer experiences and aligning people, processes and technology to deliver exceptional outcomes. At HomeStart, she leads the organisation’s customer-focussed functions, including marketing and communication, customer support, and strategic partnerships. Vas also plays a key role in shaping HomeStart’s organisational strategy and driving innovation to ensure the business continues to meet the evolving needs of South Australians. |

| Simon Olifent | Chief Financial OfficerSimon Olifent joined HomeStart as Chief Financial Officer in January 2024. He was previously at Westpac in Sydney where he worked in senior finance roles for more than 13 years, including Finance Director for the past four years. Prior to his banking experience, he was a Senior Manager of Audit and Transaction Services at global professional services firm PwC, based in Sydney and Adelaide. |

| Ryan Officer | Chief Risk OfficerRyan Officer joined HomeStart as Chief Risk Officer in October 2021. He has held roles across multiple facets of the banking sector with experience in business and retail banking in both sales and risk management. In this role, Ryan has oversight of credit and operational risk and compliance, legal, information services and products. |

| Vanessa Charlesworth | People and Capability LeaderVanessa Charlesworth joined HomeStart in 2010. She has worked as an HR professional for more than 25 years in the health and finance industries. At HomeStart, she uses her professional skills and knowledge to assist and guide the organisation strategically on a broad range of matters across a range of disciplines including employee relations, talent management, work health and safety, learning and development, recruitment and remuneration. |

Financials

HomeStart achieved an underlying profit before tax of $48.1M in 2024-25, up from $39.5M in the previous year, reflecting strong portfolio growth and a higher net interest margin. The buoyant property market underpinned significant realised and unrealised gains on HomeStart’s shared equity portfolio.

Once unrealised gains and loan provisioning changes were included, HomeStart achieved a headline profit before tax of $65.1M ($49.3M, 2023-24).

HomeStart continued to provide substantial payments to the Government, amounting to $100.6M for the year, and $1.1BN since inception in 1989. HomeStart ended the year in a strong financial position, with excellent underlying profitability, sound credit and a pipeline of growth. Combined with the organisational focus of delivering social obligations to our customers within a commercial framework and prudent risk management, HomeStart continues to ensure long-term value for all. HomeStart received a Community Service Obligation (CSO) reimbursement of $9.1M in 2024-25 ($8.8M, 2023-24) recognising the cost of providing our non-commercial activities. HomeStart’s debt funding from the South Australian Government Financing Authority (SAFA) was $3.3BN against a borrowing limit of $3.7BN, with the Treasurer approving an increase to the limit during the year (2023-24 limit of $3.4BN).

Gross loan portfolio size

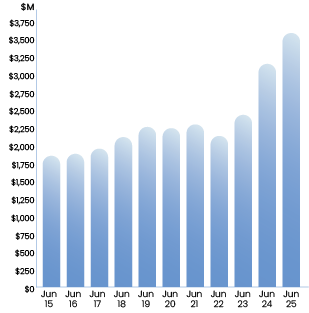

The gross loan portfolio increased during 2024-25 to $3.6BN ($3.1BN, 2023-24)

Asset and liability management

The gross loan portfolio increased during 2024-25 to $3.6BN ($3.1BN, 2023-24). While interest rates have fallen from their peak, market conditions remained challenging with elevated interest rates, rising house prices and cost of living pressures. This drove increased demand for HomeStart’s unique product offering. HomeStart delivered $1.4BN of new lending during the year ($1.2BN, 2023-24), which was a record level. The value of loans refinanced to other lenders has increased significantly this year to record levels, as customers benefit from the equity generated from strong property price growth and reductions in interest rates.

Funding

HomeStart’s lending is financed by its capital base and borrowings from SAFA. A global approach to treasury risk management continues to be applied, whereby risks are amalgamated from all activities and managed on a consolidated basis, taking advantage of offsetting risks. HomeStart’s Asset and Liability Committee (ALCO) reviews HomeStart’s Treasury policies and compliance with them.

Provisioning

HomeStart has recognised specific and collective provisions of $33.4M ($26.8M, 2023-24) against its loan portfolio, which is an increase on the prior year in line with growth in the loan portfolio.

Credit performance across the portfolio continued to be very strong. HomeStart’s customers are protected against increases in interest rates by the Repayment Safeguard, which means that loan repayments increase at or around the rate of inflation, rather than increasing in line with interest rates. This aspect of HomeStart’s loan products has helped to keep credit performance at a strong level.

Consistent with industry practice and the forward-looking nature of Australian Accounting Standards Board (AASB) 9 Financial Instruments, HomeStart retained a conservative posture in relation to provisioning for future bad and doubtful debts. This position reflects the general uncertainty surrounding the outlook for economic conditions in the coming year, with cost-of-living pressures expected to continue to present challenges for borrowers.

Management believes the sum of its specific and collective provisions constitutes adequate provisioning to meet potential loan losses in the future.

Financial indicators | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

Headline profit ($M) | 15.6 | 17.0 | 20.3 | 18.9 | 23.3 | 31.2 | 49.6 | 55.7 | 37.7 | 49.3 | 65.1 |

Net interest margin (%) | 1.0 | 1.1 | 1.3 | 1.2 | 1.3 | 1.9 | 2.2 | 2.2 | 1.8 | 2.3 | 2.5 |

Balance sheet strength | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

| Capital ($M) | 173.2 | 157.3 | 165.4 | 162.2 | 159.2 | 158.4 | 161.6 | 185.4 | 181.6 | 169.0 | 160.0 |

| Provisions ($M) | 18.0 | 17.3 | 18.2 | 17.5 | 18.6 | 23.4 | 20.6 | 19.7 | 20.6 | 26.8 | 33.4 |

| Gross loan portfolio ($M)1 | 1,840.2 | 1,867.7 | 1,939.7 | 2,103.1 | 2,245.7 | 2,227.5 | 2,280.5 | 2,119.4 | 2,415.1 | 3,131.0 | 3,563.7 |

1 Gross loan portfolio excludes Wyatt, Starter and SEO Construction products which are administered by HomeStart on behalf of the Wyatt Trust and South Australian Housing Authority (SAHA).

Financial contributions to the State Government

$1.1BN paid to the State Government since inception

Payment type ($M) | 1995-20151 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | Total |

Guarantee fee | 241.2 | 26.5 | 28.0 | 28.6 | 29.7 | 27.5 | 22.9 | 19.7 | 18.0 | 23.3 | 31.6 | 497.0 |

SAFA2 admin fee | 14.2 | 1.0 | 1.0 | 1.1 | 1.2 | 1.2 | 1.2 | 1.2 | 1.2 | 1.5 | 1.7 | 26.5 |

Tax equivalent | 67.3 | 4.9 | 5.2 | 6.2 | 6.0 | 9.0 | 11.0 | 16.0 | 16.8 | 12.9 | 19.1 | 174.4 |

Dividends | 86.9 | 7.1 | 7.1 | 9.1 | 14.8 | 22.3 | 26.2 | 46.4 | 26.1 | 32.9 | 48.2 | 327.1 |

Interim (special) dividend | 47.3 | 20.0 | 0.0 | 10.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 77.3 |

Total paid | 456.9 | 59.5 | 41.3 | 55.0 | 51.7 | 60.0 | 61.3 | 83.4 | 62.1 | 70.6 | 100.6 | 1,102.4 |

1 no payments made prior to 1995 | 2 South Australian Government Financing Authority

Contributions reflect cash payments made to the State Government during the year, and exclude any CSOs received from the State Government.

Certification of financial statements

For the year ended 30 June 2025

We certify that the:

- financial statements of HomeStart:

- are in accordance with the accounts and records of HomeStart Finance

- comply with relevant Treasurer’s Instructions; and

- comply with relevant accounting standards; and

- present a true and fair view of the financial position of HomeStart Finance at the end of the financial year and the result of its operations and cash flows for the financial year.

- internal controls employed by HomeStart Finance for the financial year over its financial reporting and its preparation of financial statements have been effective.

Signed in accordance with a resolution of the Board members.

| |  |

Jim Kouts 16 September 2025 | Andrew Mills 16 September 2025 | Simon Olifent 16 September 2025 |