Annual Report 2023-24

In the 2023-2024 financial year, we reached significant milestones, setting new records across key areas, including total lending volume, construction-related lending, loans for first home buyers, and Graduate Loans. These accomplishments illustrate our ongoing commitment to supporting more South Australians achieve their dream of home ownership.

Hear from our CEO Andrew Mills and download a copy of our latest Annual Report below.

17 September 2024

The Hon. Stephen Mullighan MP

Treasurer of South Australia

Parliament House

North Terrace

Adelaide SA 5000

Dear Treasurer,

HomeStart 2023 – 2024 Annual Report

It gives me great pleasure to present a summary of HomeStart’s achievements over the 2023-24 financial year.

HomeStart continued to make home ownership a reality for more people in more ways, assisting 2,869 households to purchase their own home.

I welcome any requests for further information should you have any questions about this report.

Yours sincerely,

Jim Kouts | Chair

What HomeStart provides isn’t just a home loan. It’s belief, hope, and possibility for those who feel home ownership is out of reach. On a daily basis, HomeStart provides a foot in the door for our customers, while over our decades in the housing market, we have delivered strong financial foundations for all South Australians.

Today, a second generation of customers, who grew up in their parents’ HomeStart-financed homes, are seeking to become homeowners themselves - at a time when the cost of living is placing home buyers under increasing pressure.

Buying a home in 2024 is very different from when HomeStart opened its doors in 1989.

Amid a national housing crisis, a wider breadth of customers are being locked out of home loans via other lenders and our purpose is as clear as ever – making home ownership a reality for more people in more ways.

The State Government has charted its Housing Roadmap to address the housing crisis in South Australia and HomeStart is delivering on its foundational role in that plan, through the success it fosters for home buyers and through its solid financial outcomes for government.

Previous policy settings came to fruition for HomeStart in 2023-24, enabling us to stand up and show up for our customers when they needed it. This is evidenced by our record $1.2 billion lending volume, equating to 2869 loans. Our 2% deposit Graduate Loan remains a runaway success and with the support of the State Government has been extended to all first home buyers building a home, which will provide ongoing support to the building and construction sector. Our Shared Equity Option has cemented itself as an additional choice for one in three of our customers to boost their borrowing power.

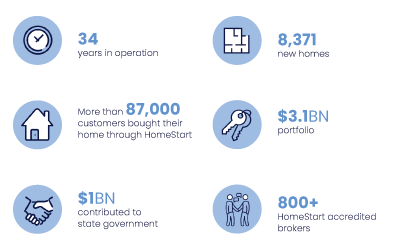

We now have a total portfolio value of $3.1 billion and have provided loans to more than 87,000 customers since HomeStart’s inception.

With an estimated 83% of our customers unable to gain finance for their home elsewhere, our customers’ average purchase price reached $515,494 up from $460,030 in 2022-23.

This snapshot of our market aligns with the trajectory of the overall housing market and illustrates the well-known recipe for challenges facing prospective home buyers.

Foreseeing that interest rates would remain higher for longer, we have run the business prudently, achieving a $39.5 million underlying profit in addition to excellent customer outcomes and a headline profit of $49.3M.

Our annual contribution to State Government was $70.3 million in another extraordinary year of delivering for all our stakeholders. This brought HomeStart’s total contribution to the State Government since its inception past the $1 billion mark.

It is worth taking a moment to acknowledge that significant financial achievement, as we head towards another milestone in the coming year - our 35th birthday.

Our strong governance and management practices remain key to our underlying strength. This governance model has enabled outstanding organisational success in the challenging times that appear to have become standard circumstances.

At the Board level, we have a strong focus on regeneration and succession, necessary to ensure we have an appropriately skilled Board with the ability to expertly govern what is now a significant financial entity.

We continually improve our efficiency by understanding where our strengths lie. Our prudent financial and risk management – and lending practices – support our financial and reputational strength, ensuring our future presence in the market. This stability in turn enables us to help more aspiring home buyers.

HomeStart’s Strategic Plan for 2024-2027 will be delivered against the backdrop of continuing challenges, with even moderate-income families now facing barriers to purchasing a home.

Unusual and conflicting economic forces have set us on a course that has diverged from recent experiences. Rising house prices, higher interest rates and the cost-of-living pressures continue to affect access to housing for renters and home buyers.

The resultant gap between affordability and entry-point homes is where HomeStart’s market is expanding.

There are understandable concerns that for low-to-moderate income households, this could be a permanent shift, so we have re-positioned towards that section of the market to keep their home ownership dream alive. It is my great pleasure to acknowledge the tremendous contribution of CEO Andrew Mills, the Executive, and the entire HomeStart team through this challenging period, and for the results achieved.

I thank my Board colleagues for their constructive perspectives and commitment to open debate about critical business issues. I also thank departing board member Paulette Kolarz for her significant contributions to the HomeStart Board and welcome Stella Thredgold and Richard Bryant, who joined us.

I also thank Treasurer Stephen Mullighan and his team for sharing our vision and supporting us with policy settings closely directed towards HomeStart’s purpose.

Lastly, I join Andrew in congratulating all who have worked over more than three decades to build HomeStart into what it is today. Our 35th birthday will be a time to reflect on an outstanding record of building opportunities for South Australians – and how we can continue to do so for a new generation.

Jim Kouts | Chair

It has been an extraordinarily challenging environment for all home buyers, and it has been essential that HomeStart acts to ensure we continue to deliver on our purpose of making home ownership a reality for more people in more ways. Our results in the past year demonstrate the significant, positive impact that HomeStart has had on creating opportunities for home buyers, and in doing so, helping relieve pressure on other components of the housing system including private rental.

Illustrating these factors, our annual lending last year reached generational highs, with the number of new loans the highest since 2006, and lending to first home buyers the highest since 2001.

We achieved a record lending volume of $1.2 billion (up 54% on last year) or 2,869 loans (up 40%) in the past year. First home buyers accounted for about two-thirds of our customers with 1,905 loans.

HomeStart’s construction related lending was also a record with 1,081 loans, including 701 loans to first home buyers. Our construction financing is estimated to have contributed to $692 million in economic activity and supported around 2,147 jobs across the broader economy. The State Government’s election commitment to make our 2% deposit home loan available to first home buyers building a home was also launched this year.

While construction and first home buyer activity were standout achievements, it is important to reiterate that HomeStart supports home buyers in many different circumstances and stages of life. Even though our lending has grown significantly, it remains resolutely focused on our target customer groups – those unable to obtain finance elsewhere.

We also provided a record number of Graduate Loans -1,142 loans, up from 924 in the previous year. Customers choosing our Shared Equity Option to boost their borrowing power accounted for about one in three new borrowers.

This significant proportion reflects growing market acceptance of the product and it has become clear that our Shared Equity Option provides one of the most important mechanisms for assisting people into home ownership.

Meanwhile, our 90-day arrears rate of 0.41% remains at near record low levels, which is a testament to our responsible lending practices, and demonstrates our customers’ commitment to maintaining their home amid cost-of-living pressures.

It is particularly pleasing to see that their commitment is demonstrably shared by our team. The HomeStart team has grown to reflect the increased demand for our loans, and notwithstanding the substantial lift in activity levels, it was welcome to learn from our recent employee surveys that our employees remain highly engaged, with engagement scores lifting to 79% this year.

Our purpose resonates strongly with our entire team, and is reflected in the difference they want to make for all our customers. During the year we also took the time to refocus our values, working to ensure that every facet of how we work with each other, our customers, and our stakeholders, reflects these values of Opportunity, Determination, Openness and Simplicity.

Even with an increase in activity levels, our growing network of more than 800 accredited mortgage brokers reported higher satisfaction levels of 71% by year end. Broker originated loans accounted for almost three-quarters of all new loans during the year.

During the year we unveiled a rebranding and new campaign called “It’s home time”. Designed to better reflect our purpose and role in the market, while also reflecting the realities of people who are working hard to achieve their home ownership dream but are feeling shut out of the market. The campaign received the highest positive response in a decade, reaching 85%, up from 66% for the previous campaign.

As we approach a new stage of the economic cycle, HomeStart is in a strong position. We have delivered some outstanding results for the community in a complex and rapidly changing economic environment, but there is still significant work to do to address the growing barriers to home ownership for our customers.

As we reflect on the challenge ahead, I thank the Treasurer and his team for their continued support and encouragement. I also wish to thank the Chair and the Board of HomeStart for their counsel, constructive challenge, and support for myself and our entire team in this latest chapter of HomeStart’s proud history.

Given the significance of the results in the year just passed, I also wish to pass on my very sincere thanks to my Executive team for their contribution and leadership, and the entire HomeStart team for their effort, care and commitment towards our organisation. I am very proud of the work they all do and look forward to continuing our shared purpose of making home ownership an affordable reality for more people in the years to come.

Andrew Mills | CEO

South Australian Government Priorities

During the 2023-24 financial year, HomeStart reported to the South Australian Treasurer, the Hon. Stephen Mullighan MP. HomeStart seeks to actively contribute towards State Government priorities including The Housing Roadmap which was launched in June 2024.

This includes:

- Helping more South Australians into their own home sooner.

- Providing more support for people to buy a home.

- Providing greater support for more new houses in the regions and greater support for regional communities.

- Greater support for homebuyers through

- HomeStart products.

As a statutory corporation operating under the Housing and Urban Development (Administrative Arrangements) (HomeStart Finance) Regulations 2020, HomeStart is empowered to:

- Facilitate home ownership in South Australia by lending and providing other forms of financial assistance, including finance on concessional or special terms for low to moderate income earners

- Provide, market, and manage home finance products and facilitate alternative schemes to encourage home ownership, including mortgage relief schemes and facilitate finance to develop community housing and aged care residential facilities.

Over the last 34 years, HomeStart has helped more than 87,000 South Australians realise their dreams of home ownership. We understand that for many, it is about more than buying a home; it is a path to financial security and freedom.

During this time, HomeStart has continued to adapt to meet our customers’ needs to support them in a rapidly changing and uncertain market, which has made it even more difficult for prospective buyers to get a foot on the property ladder.

Everyone deserves the chance to own their own home, and we are helping our customers find pathways where many lenders can’t.

Our success has not only provided direct benefits to the South Australian Government and taxpayer, but also to the State’s building and construction industries, and our rapidly expanding network of mortgage brokers.

"I feel more comfortable having a chat to HomeStart staff than any other funder I deal with. Broadly speaking, I get the impression they genuinely care about the customer, and I am sad to say, that is rare across the lenders. So, thank you." Accredited HomeStart Broker

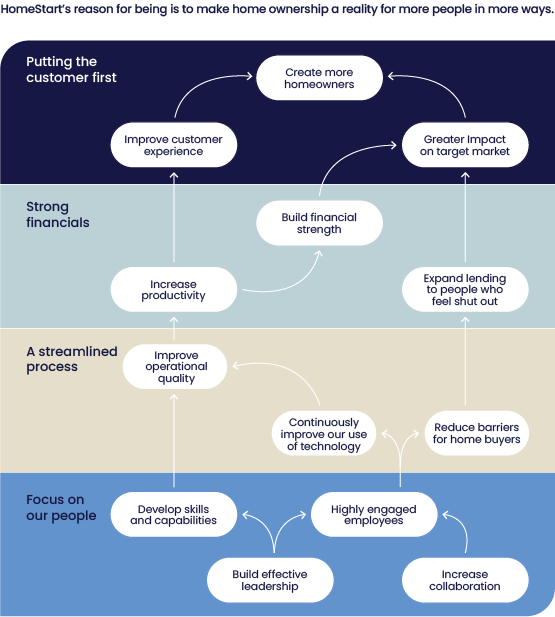

As HomeStart entered the final year of its three-year strategic plan, we remained centred on making home ownership a reality for more people in more ways.

Strong outcomes were realised across all four key areas of strategic perspectives during the year – Customer, Financial, Process and People.

HomeStart’s Strategic Plan 2024-2027

The HomeStart Strategic Plan for 2024-27 reinforces the strong sense of determination that exists within HomeStart to open doors for those who might feel shut out.

The role, relevance, and necessity of HomeStart has never been more crucial. By executing our Strategic Plan 2024-2027, we will help create thousands of new homeowners, enabling them to achieve their goals and aspirations.

HomeStart’s strategy

The strategy map illustrates our strategic priorities in the coming three years, with our people as the foundation.

Importantly, achieving our purpose of making home ownership a reality for more people in more ways is built on our values.

We believe that by building effective leadership and increasing collaboration this will lead to highly engaged employees. Building effective leadership also results in our people developing the skills and capabilities they need to succeed.

This, coupled with highly engaged employees leads to a continuously improved use of technology, and improved operational quality.

By improving operational quality, we will increase productivity which will help us build financial strength and improve the customer experience. By improving our customer experience, we will create more homeowners.

Our highly engaged employees will find ways to reduce barriers for homebuyers allowing us to expand lending to people who feel shut out. This coupled with our financial strength allows us to have a greater impact on target markets. By having a greater impact on target markets, we will create more homeowners.

HomeStart’s purpose is to make home ownership a reality for more people in more ways.

Rapid increases in house prices, higher interest rates and increasing cost of living pressures are all impacting housing accessibility for potential home buyers and renters. Over the last 12 months we’ve continued to evolve our home loan products, to keep the home ownership dream alive for more South Australians who might otherwise feel shut out of the market.

Adapting to meet our customers’ changing needs

We understand the two major obstacles for homebuyers are saving for the deposit and ensuring they have enough borrowing capacity for the home they need.

In response to the increasingly challenging housing market, we’ve continued to adapt our range of low deposit home loans and additional loan options to increase our customers borrowing power and help them manage upfront costs. Refinements to our product portfolio included:

- Extending the non-repayment period for construction loans from 9 months to 12 months

- Introducing a 2% deposit loan for first home buyers looking to build or buy a new home.

Providing certainty with repayments

Our Repayment Safeguard sets our customers’ repayments at an affordable level from the start of the loan. The repayments are then only adjusted once every 12 months in line with inflation, not when interest rates change.

This provides our customers with more repayment certainty and peace of mind over the course of the year.

No Lenders Mortgage Insurance

HomeStart doesn’t require Lenders Mortgage Insurance unlike many other lenders, saving customers tens of thousands of dollars and reducing their upfront costs.

Who we’re helping into home ownership

HomeStart is helping more customers into home ownership who are at different stages of life, in a variety of situations.

- 66% are first home buyers.

- 57% of our customers are aged between 18 and 39.

- 53% are couples, 47% are single with 12% being single parents.

- 57% had moved into their home from a private rental.

- The median gross household income was $91,600

- The average price of a metro property purchased through HomeStart was $551,000.

- The average price of a regional property purchased through HomeStart was $424,000.

- 40% of properties were purchased in Northern Adelaide, 18% in Southern Adelaide, 25% were purchased in regional areas.

"The predictability, stability and flexibility of the loans have been more helpful in the cost-of-living crisis than I could have ever imagined." - HomeStart customer.

Low deposit home loans

Our low deposit home loans are designed to help people get into home ownership sooner, with low deposits and no Lenders Mortgage Insurance.

Graduate Loan

The Graduate Loan is a low deposit loan helping people with a Certificate III qualification or higher to buy or build their own home sooner. The Graduate Loan deposit requirement for buying an established home is 2%.

1,142 Graduate Loans

$621M+ Graduate Loans value

24% Increase in number of loans from 2022-23

39% Increase in loans value from 2022-23

91% Graduate Loans issued to first home buyers

9,052 Total Graduate Loans to date

HomeStart Home Loan

The HomeStart Home Loan is a low deposit home loan (5%) for people looking to buy an existing home, build, refinance, or for buying land now and building later.

1,460 HomeStart Home Loans

$571M+ HomeStart Home Loans value

56% Increase in number of loans from 2022-23

76% Increase in loans value from 2022-23

29,167 Total HomeStart Home Loans to date

Additional loans to boost your budget

HomeStart offers a range of additional loans to increase customers’ buying power without increasing repayments. These loans provide additional funds to help with affordability and expand housing choice.

Shared Equity Option

HomeStart’s Shared Equity Option allows customers to borrow up to 25% of the purchase price as an interest-free and repayment-free loan, whether buying or building a home. In exchange for the Shared Equity Option, HomeStart shares pro rata in the capital gain or loss when the property is sold. HomeStart has offered shared equity in various forms since 2007.

889 Shared Equity Option loans

$113M+ Shared Equity Option loans value

86% Increase in number of loans from 2022-23

98% Increase in loans value from 2022-23

2,944 Total shared equity loans to date

Advantage Loan

The Advantage Loan increases low-to-moderate income earners’ buying power without increasing monthly repayments. Held in addition to another HomeStart loan, it carries a low, subsidised interest rate. Repayments start after home buyers pay off their standard HomeStart loan.

181 Advantage Loans

$6.2M+ Advantage loans value

14,609 Total Advantage loans to date

Additional loans for upfront costs

HomeStart offers a range of additional loans to help cover upfront costs like the deposit and additional fees and charges to help South Australians get into their own home sooner.

Starter Loan

The Starter Loan is designed to help cover the upfront costs of buying or building a home, such as stamp duty or conveyancing fees. The loan of up to $10,000 is taken out with another HomeStart loan and offers an interest and repayment-free period of seven years. The Starter Loan was launched in 2019.

510 Starter Loans

$4.5M+ Starter Loans value

36% Increase in loans value from 2022-23

1,760 Total Starter Loans to date

Wyatt Loan

HomeStart offers eligible low-income households a loan of up to $12,000 to assist with upfront costs, in conjunction with The Wyatt Trust. The loan is taken out with another HomeStart loan and offers an interest and repayment-free period of five years.

9 Wyatt Loans

$94k Wyatt Loans value

437 Total Wyatt Loans to date

Construction and equity loans

Helping people build and buy new homes

Many of HomeStart’s loans can be used when building or buying brand new homes. Construction Loans are repayment-free for the first twelve months or until construction is complete, whichever comes first.

1,081 Loans for construction related purposes

$423M+ Construction loans value

89% Increase in number of loans from 2022-23

97% Increase in Construction loans value from 2022-23

8,371 Total loans to date

Seniors Equity Loan

The Seniors Equity Loan allows customers aged over 60 to access part of their home’s equity as a single lump sum.

260 Seniors Equity Loans

$46M+ Seniors Equity loans value

48% Increase in number of loans from 2022-23

72% Increase in loans value from 2022-23

3,215 Total Seniors Equity Loans to date

| Net Promoter Score at June 2024 | 51 |

| Broker satisfaction score at June 2024 | 71% |

| % of customers who couldn’t get finance elsewhere | 83% |

| % of customers who took out additional loan options | 54% |

Community engagement

Seminars

HomeStart offers free educational seminars that equip attendees with the knowledge, tools, and terminology needed to confidently start their journey toward buying or building their own home.

| 2023-24 Home Buyer Seminars | 2 |

| Attendees | 325 |

Home Buyer Ready Program

Home Buyer Ready provides information to help customers get started to buy or build their own home, such as how to budget and save for a deposit, understand the costs involved, how to work out how much they can borrow and what their repayments might be.

| Users | 4,675 |

| Modules completed | 858 |

Community partnerships

- Adelaide 36ers

- Adelaide 500

- TAFE SA

- The Advertiser Teen Parliament 2024

During the 2023-24 financial year, we proudly launched our updated organisational values: Opportunity, Determination, Openness, and Simplicity.

To ensure these values are deeply understood and embraced by all employees, we conducted comprehensive training sessions and workshops. Our values have also been embedded into our regular performance review discussions.

These initiatives were designed to help our team members internalise these core values and understand how to exemplify them in their daily work. Through these efforts, we aim to create a cohesive and values-driven workplace culture that aligns with our strategic plan.

We also implemented a new performance management platform, that supports our business objectives, facilitates more frequent and effective conversations between our employees and People/Team Leaders, builds skills and competencies to grow our people more effectively and provides in-context feedback to develop our employees into high performers.

Additionally, we successfully implemented a new Learning Management System (LMS) which is designed to provide our people with virtual or in-person training they need to grow, build flexible learning spaces to drive engagement, share accurate data and deliver real time insights to analyse learning, skills and compliance trends.

To support change management activities, 94 of our employees participated in workshops on Understanding Change and Understanding Change Barriers. These sessions have been crucial in helping our workforce navigate and adapt to the changes within our organisation.

In terms of training achievements:

- Our employees dedicated a total of 645 hours to regulatory compliance training.

- 32 individuals completed the “Seven Secrets to a Healthy Mind” online course.

- 20% of our workforce remain accredited in

- Mental Health First Aid (MHFA).

- CPR training was provided to 13 employees.

- We facilitated training to 122 employees in Physical Security.

Feedback from our training programs indicates that 93.4% of participants found the information they received to be extremely helpful or helpful.

Employee engagement

- Overall average Employee Engagement Score: 79%.

Our workforce

- 54% women.

- 40% female executives.

- 8% employed part-time.

- 34% born overseas.

Leadership and management training expenditure

HomeStart invested $423,827 in training and developing its people over the course of the year equating to 2.25% of salary expenditure.

Performance management and development system

Performance plan discussions and documentation are managed through the Performance Management and Learning Management System. Our formal performance discussion process occurs every six months, with a strong emphasis on learning and growth.

Performance

As at June 30, 2024, 100% of employees had a performance development discussion in the preceding six months.

Chair

Jim Kouts has significant commercial, strategic and governance experience across a range of national and state-based private and government sector organisations. He is a former senior national executive having worked for two global energy groups for close to 20 years. Jim is a Non-Executive Director of the Adelaide Economic Development Agency, and a Non-Executive Director of Business Events Adelaide (BEA.) Until recently he was Chair of BEA. He is also a Non-Executive Director of the Adelaide Venue Management Corporation and a long-term strategic adviser to both Adelaide Airport Limited and Flinders Port Holdings. Jim was appointed Chair of HomeStart in December 2013, having previously been Deputy Chair.

Deputy Chair

Chris Ward is a professional Non-Executive Director, having had more than 30 years of broad executive experience, primarily in banking and finance. He is an Advisory Board Chair to two private companies. Chris is a former Non-Executive Director, Chair of the Risk and Audit Committee, and member of the Remuneration Committee, at the South Australian Film Corporation, a former Non-Executive Director of the Australian Dance Theatre and was an Executive Partner at UniSA. Chris was appointed to the HomeStart Board in June 2012, appointed Deputy Chair in December 2013 and is currently Chair of the Asset & Liability Committee (ALCO).

.jpg)

Board Member

Andrew Seaton is Managing Director and Chief Executive of Australian Naval Infrastructure. He has extensive finance, strategic, commercial and project management experience, having worked in banking, natural resources and defence industries for more than 30 years. Andrew previously held the roles of Chief Financial Officer at Santos Limited, Vice-President Investment Banking with Merrill Lynch and Client Director with NAB. He is a Non-Executive Director of ASX-listed Strike Energy Ltd and Rex Minerals Ltd. Andrew was appointed to the HomeStart Board in 2019 and is the Chair of the Audit & Risk Committee.

Board Member

Shanti Berggren is the General Counsel and Executive Director of Legal Services at the University of Adelaide. She is a commercial lawyer who has worked in private practice and in-house roles in Los Angeles, Singapore, and Sydney. She is also a Director of the Adelaide Football Club. Shanti was appointed to the HomeStart Board in March 2017.

Board Member

Sue Edwards is a chartered accountant and is currently a Director of Mitolo Family Farms and Executive Officer of the Mitolo Family Office. She is a former Partner at Deloitte where she specialised in providing business advice, including strategy, finance and taxation, and is a former treasury manager. She is also a member of the SA Museum Board. Sue Edwards was appointed to the HomeStart Board in December 2010.

.jpg)

Board Member

Richard Bryant brings with him over 38 years of leadership experience in the property, construction, and engineering sectors, holding high-level strategic and general management roles. His career has seen him establish and oversee businesses throughout Australia, where he has applied his considerable expertise in formulating and implementing business strategies, organisational structures, staffing, and operational systems. Additionally, Richard has contributed his leadership to various board roles within both the commercial and not-for-profit sectors. Richard was appointed to the HomeStart Board in May 2024.

Paulette Kolarz

Board Member

Paulette Kolarz is the Managing Director of BespokeHR and specialises in human resource management and leadership development. During her corporate career, Paulette supported the rebranding of Harris Scarfe after it came out of receivership in 2001. She has been previously named SA Telstra Business Woman of the Year, the SA PricewaterhouseCoopers Young Business Woman of the Year and the SA Hudson Private and Corporate Business Woman of the Year. Paulette completed her term on the Board in January 2024.

Board Attendance 2023-24

Board attendance

| Member | Eligible to attend | Meetings attended |

| J Kouts (Chair) | 11 | 11 |

| C Ward (Deputy) | 11 | 11 |

| S Berggren | 11 | 10 |

| S Edwards | 11 | 11 |

| A Seaton | 11 | 9 |

| P Kolarz | 6 | 6 |

| S Thredgold | 5 | 5 |

| R Bryant | 1 | 1 |

Asset & Liability Committee attendance

| Member | Eligible to attend | Meetings attended |

| C Ward (Chair) | 11 | 11 |

| S Berggren | 11 | 10 |

| S Edwards | 11 | 11 |

| J Kouts (Alternate member) | 11 | 0 |

Audit & Risk Committee attendance

| Member | Eligible to attend | Meetings attended |

| A Seaton (Chair) | 7 | 7 |

| S Thredgold | 3 | 3 |

| R Bryant | 1 | 1 |

| P Kolarz | 4 | 4 |

| C Ward (Alternate member) | 6 | 6 |

Andrew Mills

Chief Executive OfficerAndrew Mills started as Chief Executive Officer in January 2022, having previously held senior executive positions across the organisation over the past decade. He possesses strong financial and business acumen and has been a key contributor to the success of HomeStart, fostering strong relationships within the organisation and externally.

Andrew brings a unique focus on product innovation, digital transformation and organisational development, which will be instrumental to guide HomeStart through this challenging time in the housing market. His commitment to help more South Australians into home ownership is coupled with a belief that HomeStart can continue to play a key role in the economic and social prosperity of the State.

Vas Iannella

Chief Customer Officer

Vas Iannella joined HomeStart as Chief Customer Officer in May 2020. She has more than 15 years of retail and commercial banking experience helping to redefine customer experiences, and businesses to have the right processes and people in place to deliver the best customer outcomes. In her role at HomeStart, Vas oversees marketing and communication, customer service teams and key business partners, and leads organisational strategy and innovation.

Simon Olifent

Chief Financial Officer

Simon Olifent joined HomeStart as Chief Financial Officer in January 2024. He was previously at Westpac in Sydney where he worked in senior finance roles for more than 13 years, including Finance Director for the last four years. Prior to his banking experience, he was a Senior Manager of Audit and Transaction Services at global professional services firm PwC, based in Sydney and Adelaide.

Ryan Officer

Chief Risk Officer

Ryan Officer relocated from Queensland to join HomeStart as Chief Risk Officer in October 2021. He has held roles across multiple facets of the banking sector with experience in business and retail banking and was most recently the Chief Risk Officer Retail at Bank of Queensland. In this role, Ryan has oversight of credit and operational risk and compliance, legal, information services and products.

Vanessa Charlesworth

People and Capability Leader

Vanessa Charlesworth joined HomeStart in 2010. She has worked as an HR professional for more than 25 years in the health and finance industries. At HomeStart, she uses her professional skills and knowledge to assist and guide the organisation strategically on a broad range of matters across a range of disciplines including employee relations, talent management, work health and safety, learning and development, recruitment and remuneration.

HomeStart Finance is a statutory corporation operating under the Urban Renewal (HomeStart Finance) Regulations 2020.

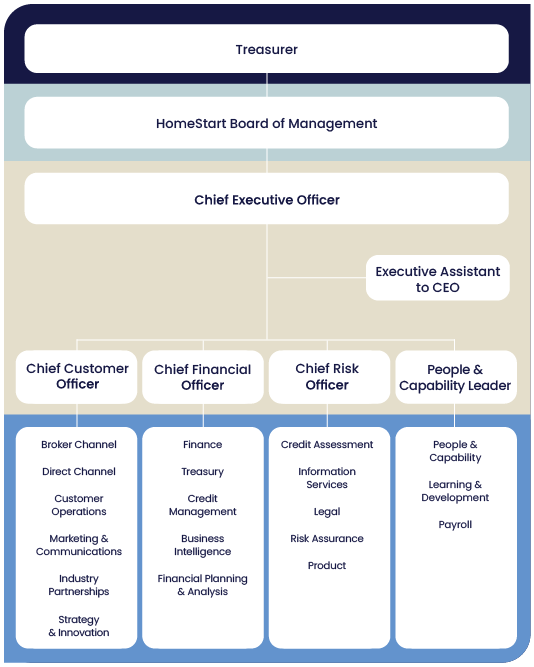

HomeStart falls under the Ministerial responsibility of the Treasurer, the Hon. Stephen Mullighan, MP in the South Australian Government. HomeStart’s approach to corporate governance is guided by legislation, State Government guidelines issued by the Department of Premier and Cabinet, Treasurer’s Instructions issued by the Department of Treasury and Finance, ASIC, and principles of best practice.

Board of Management

HomeStart is administered by a seven-member Board of Management (the Board). Board members are appointed by the Governor for a term not exceeding three years, and are entitled to such remuneration, allowances and expenses as determined by the Governor. The members who held office during 2023-24 are identified on pages 26 to 28. Board members are independent of the organisation and chosen for their expertise and skills in matters related, or complementary to, HomeStart’s business. The Board is responsible to the Treasurer for overseeing HomeStart’s business operations, with a focus on corporate accountability, strategic planning, monitoring, policy development and protecting the State Government’s financial and other interests in the organisation.

A Department of Treasury and Finance appointed observer is invited to each Board meeting. The following committees of the Board operate under individual charters and assist the Board in discharging particular functions. Committee members are selected for their expertise and independence.

Audit and Risk Committee

This committee is chaired by Andrew Seaton and membership includes two other Board members. Management personnel and representatives of the Auditor-General and internal auditors also attend meetings.

The Audit and Risk Committee’s primary responsibilities are:

- Monitoring risk management processes and status of risks and internal controls .

- Reviewing the financial reporting process and outputs.

- Reviewing compliance with relevant laws and regulations.

- Monitoring the internal and external audit functions.

- Monitoring internal control processes.

- Approving changes to the risk management framework.

- To operate in a commercial manner and manage risk prudently.

Asset and Liability Committee (ALCO)

This committee is chaired by Chris Ward and includes two other Board members plus the Chief Executive Officer (CEO) and Chief Financial Officer (CFO).

Other management personnel and representatives from the South Australian Government Financing Authority (SAFA) also attend.

The HomeStart Board has established ALCO to:

- Ensure HomeStart’s asset and liability risks are managed in a prudent manner; and

- Maintain sound, prudent financial asset and liability management frameworks and controls that result in the long term financial viability of HomeStart.

Business planning, monitoring and accountability

The Board, in conjunction with Management, establishes and reviews strategic directions and objectives for the business on an annual basis, considering external environmental factors, commercial best practice and internal aims.

These activities enable HomeStart to fulfil its purpose and deliver its long-term goals in alignment with government objectives, targets and policy directions.

The Board uses a balanced scorecard on a monthly basis to monitor all key areas of HomeStart’s business operations. The individual subcommittees of the Board provide feedback on activities undertaken in discharging the duties under their respective charters.

HomeStart incorporates appropriate risk management standards and practices into all significant new business activities or initiatives, in line with the South Australian Government’s Risk Management Policy Statement.

The Board assesses the performance of the CEO on a regular basis against current strategic and business objectives.

Board member remuneration

Member remuneration is determined by the Governor, on the advice of the Chief Executive of the Department of Premier and Cabinet. Board member remuneration information is provided in Note 8 to the financial statements.

Board member benefits

During or since the 2023-24 financial year, no Board member has received or become entitled to receive a personal benefit (other than a remuneration benefit included in Note 8 to the financial statements) because of a contract made with HomeStart by:

- The Board member.

- Any organisation of which the Board member is a member.

- Any entity in which the Board member has a substantial financial interest.

- An associate of the Board member.

Executive appointment and remuneration

Responsibility for the appointment of the CEO rests with the Board. Responsibility for executive appointments rests with the CEO. Details of executive remuneration are set out in Note 7 to the financial statements.

Risk management

HomeStart has an enterprise-wide approach to managing risks to ensure they are identified and managed at all levels of our operations.

While oversight of risk management remains the primary responsibility of the Board, each committee has specific roles and responsibilities in relation to risk management. The Audit and Risk Committee monitors all operational risks, including a regular review of the areas of highest risk. The Asset and Liability Committee (ALCO) monitors all credit and market risks.

Risk management is an integral part of everyday work and is supported by:

- An Assurance Framework that outlines how risk is managed at HomeStart.

- A Risk & Compliance Management Policy that provides the roles and responsibilities for each of the three lines; employees, Risk Assurance, and independent assurance such as Internal Audit.

- A Risk Appetite Statement summarising HomeStart’s tolerance against various risk indicators.

- Identification, assessment (using AS/NZS ISO 31000:2018) and recording of risks and controls through a risk management system.

- Continuous monitoring and reassessment of risks and internal controls, prompted by our risk management system’s interactive email capability and through regular discussion at executive and team level.

- Organisation-wide feedback on existing and emerging risks.

- Comprehensive reporting to Executive Committee, Audit and Risk Committee and Board.

Strategic risk

Discussion and assessment of risks and opportunities form part of our strategic and business planning process to enable us to prioritise objectives, maximise outcomes and mitigate threats. Our planning considers our external environment, market context, ministerial and government objectives as well as internal capabilities.

Risk and control self-assessments are conducted for each division against the strategy to ensure current risks are captured and monitored or mitigated.

Credit risk

Credit risk is inherent in HomeStart’s core function of lending. Lending policies are founded on sound credit risk management and behavioural intelligence, which is incorporated into each stage of a customer’s loan application and ongoing loan management.

Analysis is underpinned by credit risk systems that have been developed using a combination of theory and experience, drawn from the behaviour of our customer base.

Regular and comprehensive reporting and monitoring is provided to ALCO, Audit and Risk Committee and Board.

Market risk

A comprehensive set of policies govern HomeStart’s funding and interest rate risk management activities. These policies are monitored by ALCO at its monthly meetings and regularly by the Chief Financial Officer. HomeStart’s funding is entirely sourced from the South Australian Government via the South Australian Government Financing Authority (SAFA), so the exposure to market risk is limited to SAFA’s exposure.

Operational risk

Operational risks are those inherent in the day-to-day functions of HomeStart. The risk management system facilitates a comprehensive assessment, communication and monitoring framework for these risks. Management regularly reviews its risk profiles to ensure appropriate internal controls are in place and operating effectively. Any incidents that occur are recorded against the relevant risk and are investigated and mitigated where possible, within set timeframes dependent on the risk rating.

Information security risk management

HomeStart has a Cyber Security Program to safeguard against information security risks as outlined in the standard ISO/IEC 27001:2013 Information Security Management. The program includes a suite of policies specific to information security.

The Board is responsible for overseeing HomeStart’s compliance performance. The Audit and Risk Committee, in its key role of assisting the Board to fulfil its corporate governance objectives, is responsible for monitoring and reviewing HomeStart’s compliance performance.

Compliance, internal control and assurance

HomeStart’s organisational compliance framework supports the identification and assessment of our legal obligations and management and monitoring of our compliance responsibilities on an ongoing basis. This framework is reviewed on a regular basis to reflect any relevant legislative changes or any organisational structure and subsequent role changes.

HomeStart’s Board is responsible for ensuring robust and effective internal controls exist to minimise the risks inherent in our business. Internal controls are regularly reviewed in line with the Assurance Framework and Control Testing Methodology to ensure their effectiveness and to identify any assurance gaps and areas of improvement.

An Anti-Money Laundering and Counter Terrorism Financing Program is in place with suspicious matters reported to the Australian Transaction Reports and Analysis Centre (AUSTRAC).

While internal fraud is a risk that HomeStart is exposed to in various areas of the business, no inappropriate activity has been identified.

Strategies to prevent fraud are in place at all levels of our operations including:

- A register of delegations.

- An internal audit program.

- Segregation of duties.

- Dual controls in appropriate areas.

- Internal policies, procedures, monitoring and reconciliation.

- Regular and ongoing compliance training for all employees.

- A Fraud Governance Control Plan.

- Public Interest Disclosure process.

- A strong internal culture and organisational values.

Internal and external audit

External audit is undertaken by the Audit Office of South Australia and an Independent Auditors Report is provided to the Board. The report for this financial year can be found on page 74.

Deloitte conducted the operational internal audit function for 2023-24 which was based on a three-year rolling audit plan.

Freedom of Information Act 1991 – Information Statement

HomeStart Finance is a statutory corporation, established by regulation under the Urban Renewal Act 1995 to facilitate home ownership opportunities for South Australians, with a particular focus on low-to-moderate income households. HomeStart operates in a commercial manner to achieve financial and other performance benchmarks that are established and agreed with the State Government.

Policy documents

The following policy documents are held by HomeStart and are available on request free of charge:

- HomeStart home loan brochures.

- HomeStart guide to fees and charges.

- HomeStart Privacy Policy.

- HomeStart Credit Reporting Policy.

- HomeStart Annual Report.

- HomeStart Target Market Determinations.

Copies of these documents can be accessed from homestart.com.au or by contacting the Freedom of Information Officer on (08) 8203 4750.

Access to personal information

Customers are entitled to obtain access to their personal information held by HomeStart in accordance with the Freedom of Information Act 1991. HomeStart may deny a request for access if required, obliged or authorised to do so under any applicable law, including the Freedom of Information Act 1991. Any request for access to personal information must be in writing and must be sent to the Freedom of Information Officer.

HomeStart will respond to all requests for information under the Freedom of Information Act 1991 within 30 days of receipt of the request. Fees and charges may be payable.

Public Interest Disclosure Act 2018

No public interest information has been disclosed to a responsible officer of HomeStart Finance under the Public Interest Disclosure Act 2018 (SA).

Overseas travel

There was no overseas travel undertaken during 2023-24.

Work Health & Safety (WHS)

HomeStart is dedicated to maintaining a safe, injury-free workplace and fostering high employee engagement. We consistently meet key Work Health and Safety (WHS) legislation requirements and keep our WHS Manual up-to-date with legislative changes and regular reviews. Our robust Safety Management System systematically manages safety risks, enhances safety practices, demonstrates corporate due diligence, and strengthens our overall safety culture.

Activities that support a safe work environment include:

- Regular training sessions on emergency procedures.

- Ongoing education for new employees.

- Onsite refresher and/or training of Mental Health First Aid Officers.

- First Aid Officers training.

- Emergency evacuation drills.

- Annual influenza vaccination program.

- Skin check program.

- Bowel cancer screening program.

- Provision of online training; mandatory and optional opportunities.

- Choice of Employee Assistance Program providers.

- Undertaking risk assessment and hazard identification by way of worksite inspections across all locations.

- Ergonomic assessments, in the workplace and work from home employees.

- Healthy Minds Wellbeing Index measured.

- Implementation of wellbeing initiatives that promote physical and mental wellbeing.

- Ongoing maintenance of facilities and equipment.

There were no WHS Prosecutions, notices or corrective actions during 2023-24.

Public complaints

Complaints received through the Australian Financial Complaints Authority

| Collections | 6 |

| Policy | 4 |

| Service | 2 |

| Collections Policy Service Complaints lodged with State Ombudsman | 0 |

Complaints direct to HomeStart

| Collections | 2 |

| Policy | 8 |

| Service | 40 |

| Communication/Privacy | 6 |

Total complaints | 68 |

HomeStart is committed to conducting its business in accordance with the law as well as best practice and Australian Standards. Consistent with this commitment, HomeStart’s Complaints Management Policy is guided by AS/NZS ISO 10002-2022 Guidelines for complaints management in organisations and ASIC’s Regulatory Guide 271 – Internal Dispute Resolution.

A customer complaint register provides valuable information and feedback to ensure policies and procedures remain current.

Consultancy expense

| Consultant | Purpose of consultancy | Number | Cost $’000 |

|---|---|---|---|

| Total consultancies below $10,000 | |||

| Various | - | 1 | 2 |

| Total consultancies $10,000 and above | |||

| Bee Squared Consultants | Credit Process Optimisation | 1 | 90 |

| Brett & Watson | Actuary Review | 1 | 20 |

| Deloitte Touche Tohmatsu | Business Intelligence Architecture Review Capital Structure Review | 2 | 51 148 |

| Ernst & Young | Accounting Advice – Shared Equity Option | 1 | 97 |

Total consultancies | 6 | 408 |

HomeStart achieved an underlying profit before tax of $39.5M in 2023-24, up from $33.6M in the previous year, reflecting strong portfolio growth and a higher net interest margin. The buoyant property market underpinned significant unrealised gains on HomeStart’s shared equity portfolio. Once unrealised gains and loan provisioning changes were included, HomeStart achieved a headline profit before tax of $49.3M ($37.7M 2022-23). This represented a return on equity of 28%.

HomeStart continued to provide substantial payments to the Government, amounting to $70.6M for the year, and $1.0BN since inception in 1989.

HomeStart ended the year in a strong financial position, with excellent underlying profitability, sound credit and a robust pipeline of growth. Combined with the organisational focus of delivering social obligations to our customers within a commercial framework and prudent risk management, HomeStart continues to ensure long-term value for all.

HomeStart received a Community Service Obligation (CSO) reimbursement of $8.8m in 2023-24 ($5.2M, 2022-23) recognising the cost of providing our non-commercial activities. HomeStart’s debt funding from SAFA was $2.9BN against a borrowing limit of $3.4BN, with the Treasurer approving an increase to the limit during the year (2022-23 limit of $2.8BN).

Asset and liability management

The gross loan portfolio increased during 2023-24 to $3.1BN ($2.4BN, 2022-23). Market conditions of high interest rates, rising house prices, cost of living pressures and tighter lending conditions drove increased demand for HomeStart’s unique product offering. HomeStart delivered $1.2BN of new lending during the year ($0.8BN, 2022-23), which was a record level.

The value of loans refinanced to other lenders has increased this year, as customers benefit from the equity generated from strong property price growth.

Funding

HomeStart’s lending is financed by its capital base and borrowings from SAFA. A global approach to treasury risk management continues to be applied, whereby risks are amalgamated from all activities and managed on a consolidated basis, taking advantage of offsetting risks.

HomeStart’s Asset and Liability Committee (ALCO) reviews HomeStart’s Treasury policies and compliance with them.

Provisioning

HomeStart has recognised specific and collective provisions of $26.8M ($20.6M, 2022-23) against its loan portfolio, which is an increase on the prior year in line with growth in the loan portfolio.

Credit performance across the portfolio continued to be very strong. HomeStart’s customers are protected against increases in interest rates by the Repayment Safeguard, which means that loan repayments increase at or around the rate of inflation, rather than increasing in line with interest rates. This aspect of HomeStart’s loan products has helped to keep credit performance at a strong level.

Consistent with industry practice and the forward-looking nature of AASB 9 Financial Instruments, HomeStart retained a conservative posture in relation to provisioning for future bad and doubtful debts. This position reflects the general uncertainty surrounding the outlook for economic conditions in the coming year, with cost of living pressures expected to continue to present challenges for borrowers.

Management believes the sum of its specific and collective provisions constitutes adequate provisioning to meet potential loan losses in the future.

| Financial Indicators | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|---|---|---|---|

| Headline Profit ($M) | 15.6 | 17.0 | 20.3 | 18.9 | 23.3 | 31.2 | 49.6 | 55.7 | 37.7 | 49.3 |

| Return On Equity (%) | 9.0 | 10.2 | 12.5 | 11.5 | 14.4 | 19.6 | 31.0 | 32.1 | 20.5 | 28.1 |

| Net Interest Margin (%) | 1.0 | 1.1 | 1.3 | 1.2 | 1.3 | 1.9 | 2.2 | 2.2 | 1.8 | 2.3 |

| Balance Sheet Strength | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|---|---|---|---|---|---|

| Capital ($M) | 173.2 | 157.3 | 165.4 | 162.2 | 159.2 | 158.4 | 161.6 | 185.4 | 181.6 | 169.0 |

| Provisions ($M) | 18.0 | 17.3 | 18.2 | 17.5 | 18.6 | 23.4 | 20.6 | 19.7 | 20.6 | 26.8 |

| Gross loan portfolio ($M) | 1,840.2 | 1,867.7 | 1,939.7 | 2,103.1 | 2,245.7 | 2,227.5 | 2,280.5 | 2,119.4 | 2,415.1 | 3,131.0 |

Financial contributions to the State Government

$1BN paid to the State Government since inception

| Payment Type ($M) | 1995-20151 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Guarantee fee | 241.2 | 26.5 | 28.0 | 28.6 | 29.7 | 27.5 | 22.9 | 19.7 | 18.0 | 23.3 | 465.3 |

| SAFA² admin fee | 14.2 | 1.0 | 1.0 | 1.1 | 1.2 | 1.2 | 1.2 | 1.2 | 1.2 | 1.5 | 24.8 |

| Tax Equivalent | 67.3 | 4.9 | 5.2 | 6.2 | 6.0 | 9.0 | 11.0 | 16.0 | 16.8 | 12.9 | 155.3 |

| Dividends | 86.9 | 7.1 | 7.1 | 9.1 | 14.8 | 22.3 | 26.2 | 46.4 | 26.1 | 32.9 | 278.9 |

| Special Dividend | 47.3 | 20.0 | 0.0 | 10.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 77.3 |

| Total paid | 456.9 | 59.5 | 41.3 | 55.0 | 51.7 | 60.0 | 61.3 | 83.4 | 62.1 | 70.6 | 1,001.7 |

1 no payments made prior to 1995 | 2 South Australian Government Financing Authority

Certification of the Financial Statements

For the year ended 30 June 2024, We certify that the financial statements of HomeStart:

- are in accordance with the accounts and records of HomeStart Finance;

- comply with relevant Treasurer’s instructions;

- comply with relevant accounting standards; and

- present a true and fair view of the financial position of HomeStart Finance at the end of the financial year and the result of its operations and cash flows for the financial year.

- internal controls employed by HomeStart Finance for the financial year over its financial reporting and its preparation of financial statements have been effective.

Signed in accordance with a resolution of the board members.